Back

Back

Raya App, Saving & Pinang Customer Experience Design 2025

Raya App, Saving & Pinang Customer Experience Design 2025

Background

Background

Micro, Small, and Medium Enterprises (MSMEs) are one of the key pillars of Indonesia's economy. According to data from the Ministry of Cooperatives and SMEs, MSMEs contribute approximately 60% of Indonesia's total Gross Domestic Product (GDP) and employ more than 97% of the country's workforce.

Micro, Small, and Medium Enterprises (MSMEs) are one of the key pillars of Indonesia's economy. According to data from the Ministry of Cooperatives and SMEs, MSMEs contribute approximately 60% of Indonesia's total Gross Domestic Product (GDP) and employ more than 97% of the country's workforce.

Despite their significant role in the economy, many MSME entrepreneurs still face various challenges, particularly in financial literacy.

Despite their significant role in the economy, many MSME entrepreneurs still face various challenges, particularly in financial literacy.

A report by the Indonesian Employers Association (APINDO) reveals that around 60% of MSME owners lack confidence in managing finances and investments for their businesses. A lack of understanding of basic financial literacy concepts, such as financial record-keeping, budget planning, and loan management, often leads to poor financial decision-making. This poses risks of hindering business growth, reducing operational efficiency, and even causing significant financial losses.

A report by the Indonesian Employers Association (APINDO) reveals that around 60% of MSME owners lack confidence in managing finances and investments for their businesses. A lack of understanding of basic financial literacy concepts, such as financial record-keeping, budget planning, and loan management, often leads to poor financial decision-making. This poses risks of hindering business growth, reducing operational efficiency, and even causing significant financial losses.

Goals

Goals

As a digital bank focusing on the micro and small business segments, Bank Raya plays a crucial role in providing inclusive financial solutions for MSMEs. With a range of products such as personal accounts, business accounts, productive loans (Pinang Dana Talang, Pinang Maksima), and consumer loans (Pinang Flexi), Bank Raya is committed to supporting MSMEs in enhancing their financial literacy and financial management capabilities.

As a digital bank focusing on the micro and small business segments, Bank Raya plays a crucial role in providing inclusive financial solutions for MSMEs. With a range of products such as personal accounts, business accounts, productive loans (Pinang Dana Talang, Pinang Maksima), and consumer loans (Pinang Flexi), Bank Raya is committed to supporting MSMEs in enhancing their financial literacy and financial management capabilities.

Despite their significant role in the economy, many MSME entrepreneurs still face various challenges, particularly in financial literacy.

Despite their significant role in the economy, many MSME entrepreneurs still face various challenges, particularly in financial literacy.

📈 Objective

📈 Objective

Identifying the needs and challenges of MSMEs in financial literacy, including financial planning, record-keeping, loan management, and business investment.

Exploring how Bank Raya's digital solutions can address these challenges effectively.

Developing an effective service model or digital platform to enhance financial literacy and boost MSME entrepreneurs' confidence in managing their finances.

Formulating recommendations for Bank Raya to expand its digital financial services for MSMEs.

Identifying the needs and challenges of MSMEs in financial literacy, including financial planning, record-keeping, loan management, and business investment.

Exploring how Bank Raya's digital solutions can address these challenges effectively.

Developing an effective service model or digital platform to enhance financial literacy and boost MSME entrepreneurs' confidence in managing their finances.

Formulating recommendations for Bank Raya to expand its digital financial services for MSMEs.

Project Scope

Project Scope

Collaborate with stakeholders at Bank Raya and serve as the leader for the 2025 Raya App, Saving & Pinang Customer Experience Design.

Understand user and competitor behavior to design a user-centric application through activities such as discovery, defining value propositions, ideation, UI/UX design development, and release-quality design monitoring.

Develop the application using Agile methodology, ensuring product development is adaptive and responsive to changes.

Work with Bank Raya's internal team and third-party partners appointed by Bank Raya to execute the project collaboratively.

Accommodate timelines and additional requirements that align with project needs.

Collaborate with stakeholders at Bank Raya and serve as the leader for the 2025 Raya App, Saving & Pinang Customer Experience Design.

Understand user and competitor behavior to design a user-centric application through activities such as discovery, defining value propositions, ideation, UI/UX design development, and release-quality design monitoring.

Develop the application using Agile methodology, ensuring product development is adaptive and responsive to changes.

Work with Bank Raya's internal team and third-party partners appointed by Bank Raya to execute the project collaboratively.

Accommodate timelines and additional requirements that align with project needs.

Solutions

Solutions

✨ Double Diamond Approach

✨ Double Diamond Approach

✨ Research Framework

✨ Research Framework

Awareness of Financial Literacy & Management for MSMEs

Awareness of Financial Literacy & Management for MSMEs

Financial literacy is the knowledge and understanding of financial concepts and risks, as well as the skills, motivation, and confidence to apply that understanding (OECD/INFE, 2018). Financial literacy is measured based on three dimensions:

Financial knowledge

Financial behavior

Financial attitude

Financial literacy is the knowledge and understanding of financial concepts and risks, as well as the skills, motivation, and confidence to apply that understanding (OECD/INFE, 2018). Financial literacy is measured based on three dimensions:

Financial knowledge

Financial behavior

Financial attitude

Research Objective

Research Objective

To understand the differences in financial literacy levels across MSME segments and business locations in order to provide an approach/product that meets their specific needs.

Identify the key factors that make Raya Bisnis products a financial solution for MSMEs.

To understand the differences in financial literacy levels across MSME segments and business locations in order to provide an approach/product that meets their specific needs.

Identify the key factors that make Raya Bisnis products a financial solution for MSMEs.

Research Questions

Research Questions

What types of financial products are known and used by MSME entrepreneurs?

How does the implementation and impact of financial record-keeping affect business sustainability?

What are the needs and challenges faced by MSMEs in using financial products (business accounts/loans/investments) to support business operations?

How do entrepreneurs analyze risks/opportunities before making major financial decisions for their business?

What types of financial products are known and used by MSME entrepreneurs?

How does the implementation and impact of financial record-keeping affect business sustainability?

What are the needs and challenges faced by MSMEs in using financial products (business accounts/loans/investments) to support business operations?

How do entrepreneurs analyze risks/opportunities before making major financial decisions for their business?

New Feature Testing

New Feature Testing

Background

Background

In the context of launching new features on business accounts, usage testing is necessary to evaluate whether the product design provides a positive experience for users. Usability testing can be conducted through two approaches: qualitative and quantitative.

In the context of launching new features on business accounts, usage testing is necessary to evaluate whether the product design provides a positive experience for users. Usability testing can be conducted through two approaches: qualitative and quantitative.

Qualitative usability testing to study user difficulties and behavior.

Quantitative usability testing to measure success rates, average completion time, and satisfaction levels when using new features on Bank Raya's business accounts.

Qualitative usability testing to study user difficulties and behavior.

Quantitative usability testing to measure success rates, average completion time, and satisfaction levels when using new features on Bank Raya's business accounts.

Objective

Objective

This testing aims to identify weaknesses or deficiencies in the product design before launch, allowing improvements to be made to enhance the user experience and user satisfaction.

This testing aims to identify weaknesses or deficiencies in the product design before launch, allowing improvements to be made to enhance the user experience and user satisfaction.

Usability testing will be conducted in phases, testing several modules.

Usability testing will be conducted in phases, testing several modules.

💡 Onboarding Product Knowledge

💡 Onboarding Product Knowledge

MSMEs with low financial literacy are vulnerable to fraud.

MSMEs with low financial literacy are vulnerable to fraud.

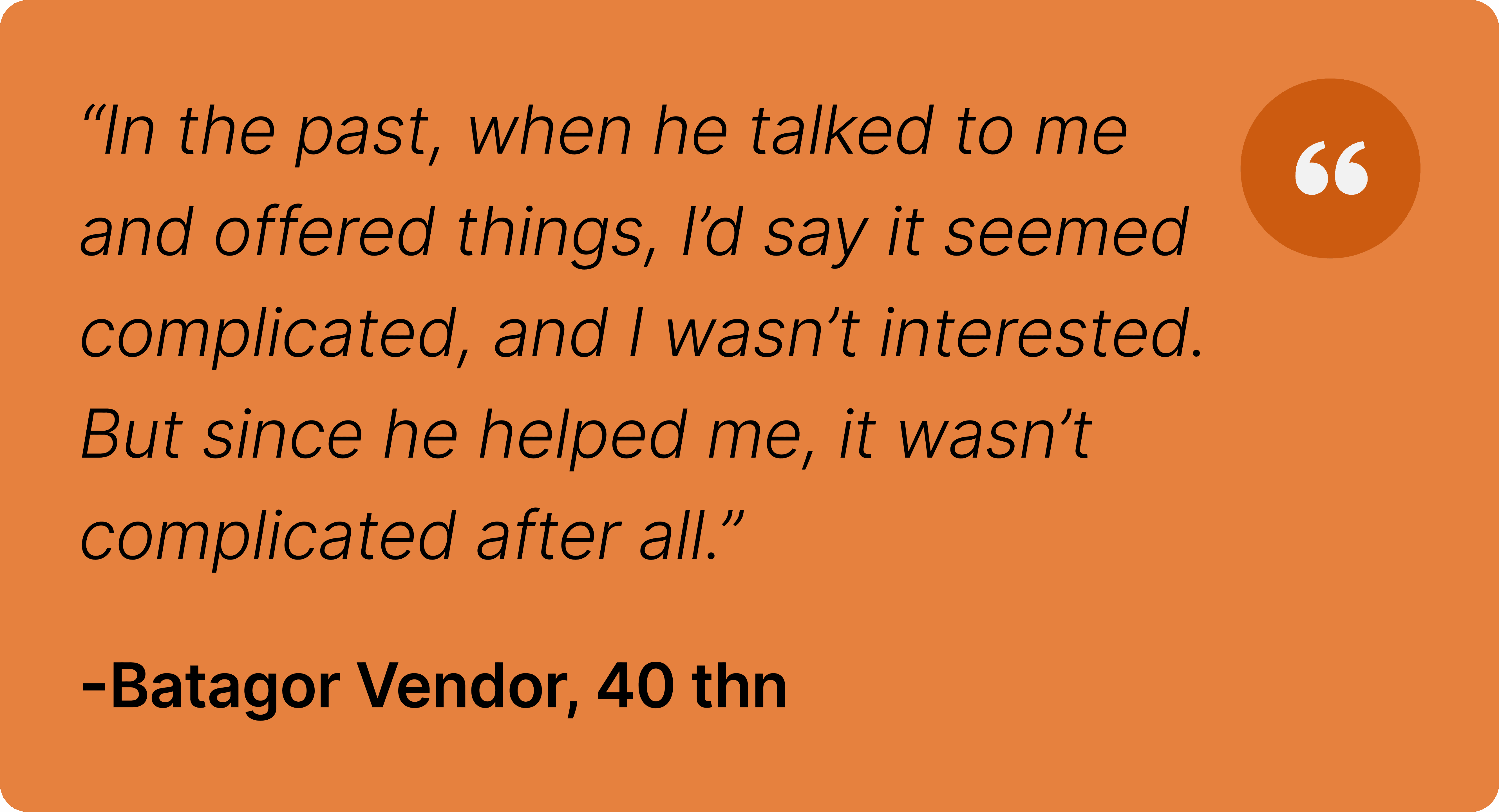

The low financial literacy among MSMEs in Indonesia is often caused by a lack of knowledge about trustworthy financial products and services. Many business owners access financial services without adequate understanding, making them vulnerable to fraud or the use of illegal financial services.

The low financial literacy among MSMEs in Indonesia is often caused by a lack of knowledge about trustworthy financial products and services. Many business owners access financial services without adequate understanding, making them vulnerable to fraud or the use of illegal financial services.

In addition, MSMEs with low financial literacy are also more susceptible to the allure of illegal online loans offering easy disbursement and illegal investments promising high returns.

In addition, MSMEs with low financial literacy are also more susceptible to the allure of illegal online loans offering easy disbursement and illegal investments promising high returns.

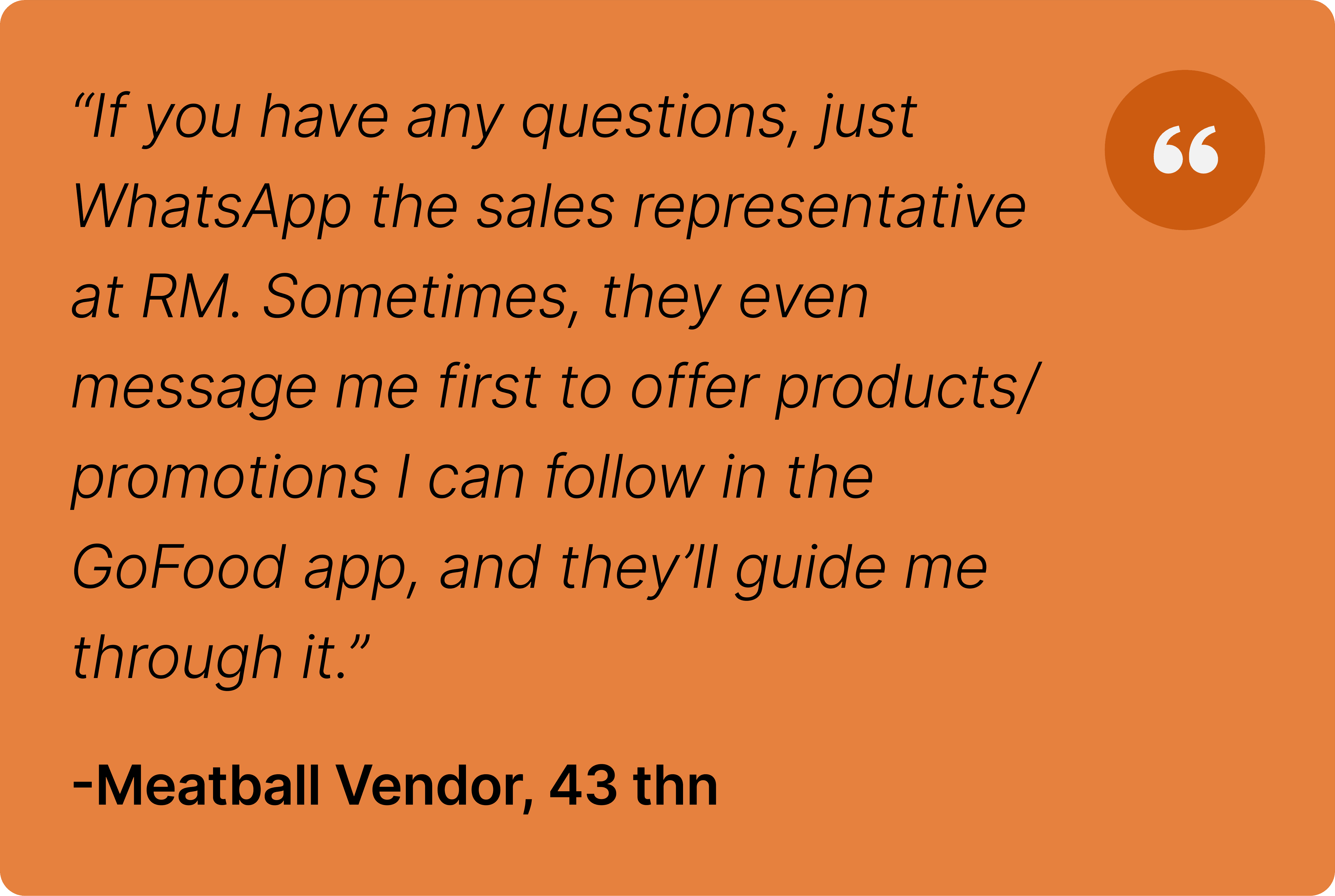

To address this issue, it is essential to introduce Bank Raya's financial products that can support MSME businesses, while also providing education about financial security through monitored communication channels, such as the official Bank Raya WhatsApp, after the creation of a Raya Bisnis account."

To address this issue, it is essential to introduce Bank Raya's financial products that can support MSME businesses, while also providing education about financial security through monitored communication channels, such as the official Bank Raya WhatsApp, after the creation of a Raya Bisnis account."

💡 Business Financial Analysis

💡 Business Financial Analysis

MSMEs are accustomed to evaluating business income and expenses.

MSMEs are accustomed to evaluating business income and expenses.

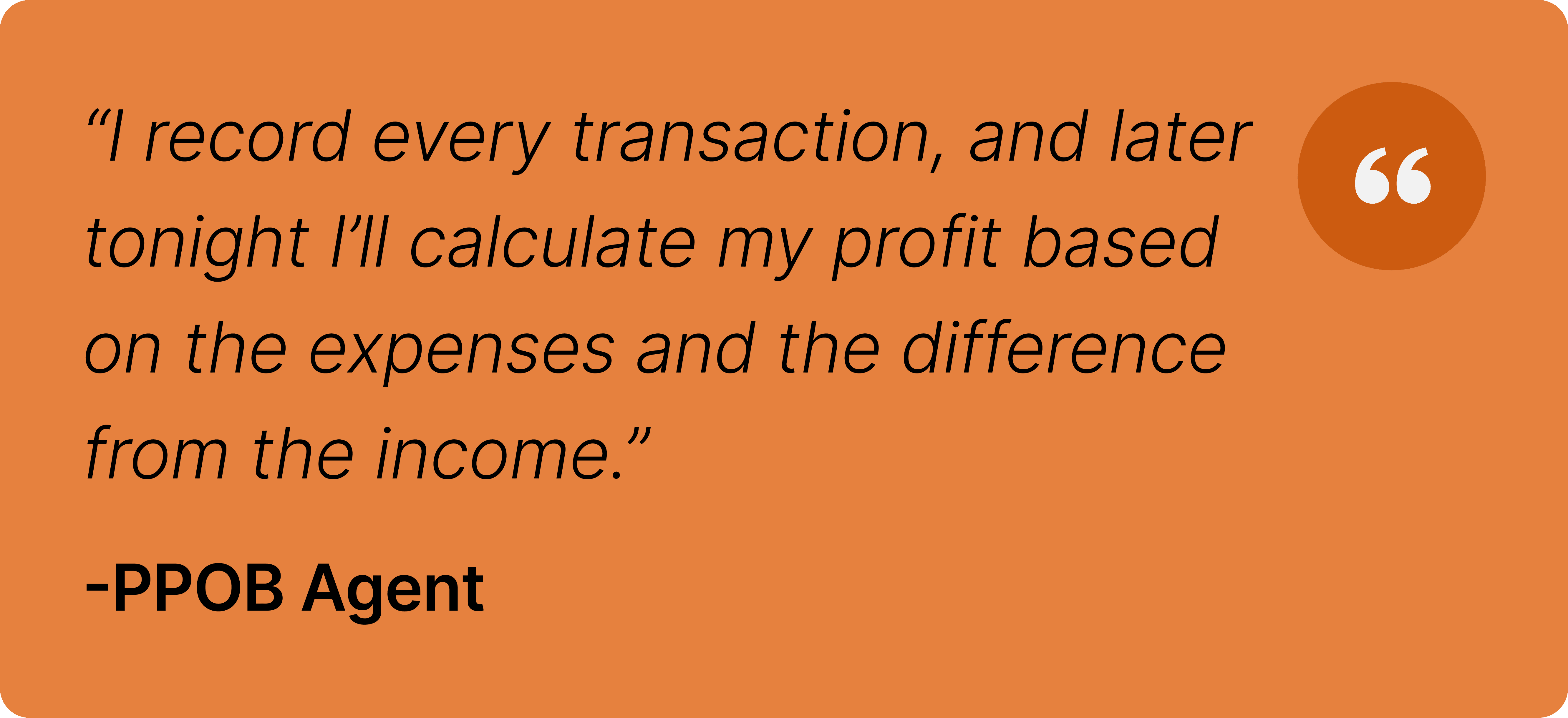

Evaluating business income and expenses is crucial for MSMEs to develop more effective business strategies. MSMEs usually set a daily sales target based on the initial capital when they start their business. Some MSMEs still manually record their total daily income to assess their business performance and then evaluate the performance at the end of the week and month.

Evaluating business income and expenses is crucial for MSMEs to develop more effective business strategies. MSMEs usually set a daily sales target based on the initial capital when they start their business. Some MSMEs still manually record their total daily income to assess their business performance and then evaluate the performance at the end of the week and month.

Evaluating income and expenses becomes more practical with the QRIS Merchant feature connected to the Raya Bisnis account. MSMEs no longer need to manually record transactions, as all QRIS transactions are automatically and real-time recorded in the system. This helps MSMEs monitor daily revenue, analyze business performance, and develop business strategies more efficiently.

Evaluating income and expenses becomes more practical with the QRIS Merchant feature connected to the Raya Bisnis account. MSMEs no longer need to manually record transactions, as all QRIS transactions are automatically and real-time recorded in the system. This helps MSMEs monitor daily revenue, analyze business performance, and develop business strategies more efficiently.

Financial record-keeping is a challenging task for MSME owners, especially those with low financial literacy.

Financial record-keeping is a challenging task for MSME owners, especially those with low financial literacy.

Maintaining organized financial records is a key requirement for MSMEs aiming to grow further. According to research, the majority of MSMEs possess good financial literacy; however, their financial management practices remain inadequate (Findy, Endang, Adam, 2024).

Maintaining organized financial records is a key requirement for MSMEs aiming to grow further. According to research, the majority of MSMEs possess good financial literacy; however, their financial management practices remain inadequate (Findy, Endang, Adam, 2024).

Many MSME owners rely solely on memory, without proper administrative record-keeping or separation of business and personal finances (Aza, Iqbal, Asep, 2024).

Many MSME owners rely solely on memory, without proper administrative record-keeping or separation of business and personal finances (Aza, Iqbal, Asep, 2024).

This issue highlights that financial record-keeping remains a challenge. Therefore, education and simplification of the financial recording process are necessary to help MSMEs better manage their finances.

This issue highlights that financial record-keeping remains a challenge. Therefore, education and simplification of the financial recording process are necessary to help MSMEs better manage their finances.

Source

Aza, Iqbal, Asep (2024 Juni, 1). Peningkatan Literasi Keuangan Pada UMKM Dusun Cibereum Desa Buanajaya Melalui Penyuluhan Laporan Keuangan Sederhana

Findy, Endang, Adam (2024 April, 3). Pengaruh Literasi Keuangan Terhadap Pengelolaan Keuangan UMKM Di Kecamatan Mampang Prapatan Jakarta

Business Financial Management

Business Financial Management

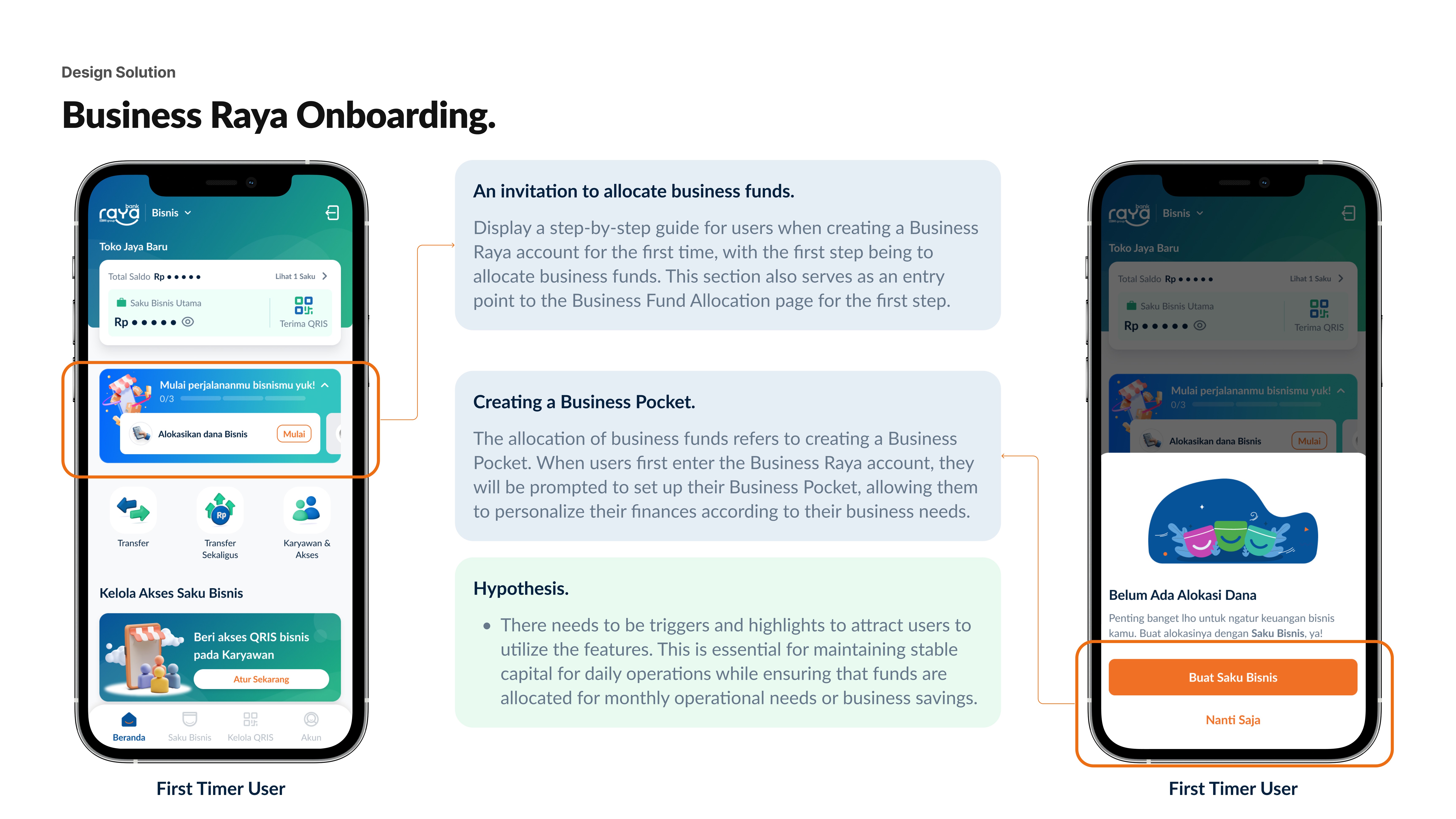

Managing financial allocations with discipline impacts business sustainability, particularly in capital and profit management.

Managing financial allocations with discipline impacts business sustainability, particularly in capital and profit management.

Based on a survey from previous research, 56.5% of F&B MSMEs are accustomed to separating their daily income between business capital and leftover profits. This habit enables them to maintain stable capital for daily operations while ensuring funds are allocated for monthly operational needs or business savings. With structured financial management, MSMEs can minimize the risk of funding shortages, prepare for business expansion, and build a stronger financial foundation for the long term.

Based on a survey from previous research, 56.5% of F&B MSMEs are accustomed to separating their daily income between business capital and leftover profits. This habit enables them to maintain stable capital for daily operations while ensuring funds are allocated for monthly operational needs or business savings. With structured financial management, MSMEs can minimize the risk of funding shortages, prepare for business expansion, and build a stronger financial foundation for the long term.